Table of Contents

The 50/30/20 budget rule is one of the most popular, easy-to-understand frameworks for managing personal finances. Whether you are just starting out on your financial journey or looking for a simple method to regain control over your money, this rule provides a clear guideline on how to allocate your income to cover your essential needs, enjoy life’s extras, and build a secure financial future.

Also Read: The Essential Role of an Emergency Fund

In this comprehensive guide, we will break down what the 50/30/20 rule is, explain its benefits and limitations, provide real-world examples and actionable advice, and offer tips for tailoring the rule to your unique circumstances. We will also answer common questions in our FAQ section and include a sample budget table to help you visualize your financial plan.

Introduction

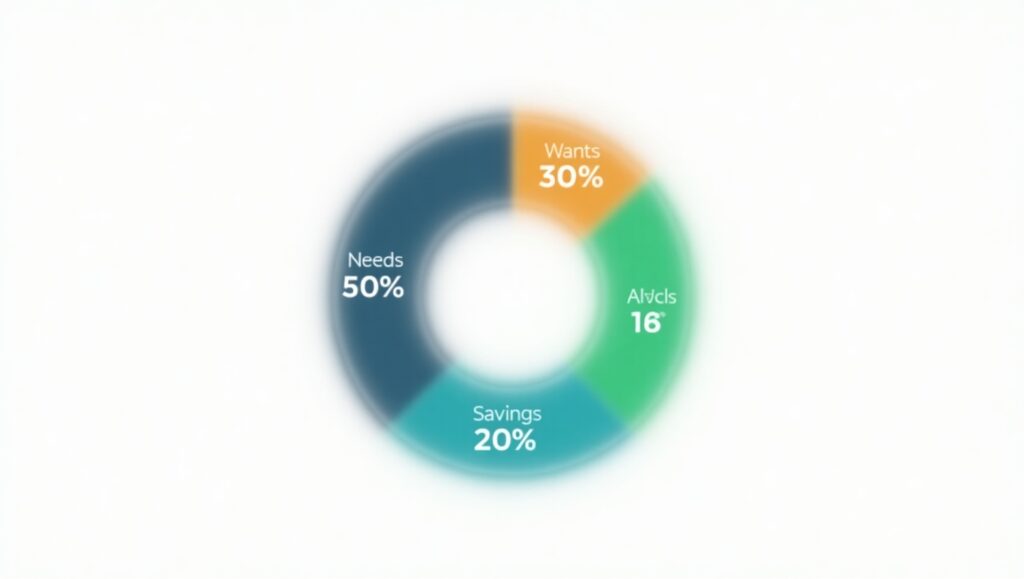

Budgeting is the foundation of effective money management. Without a clear plan for how to spend, save, and invest your money, it is easy to fall into patterns of overspending or under-saving. The 50/30/20 rule simplifies budgeting by dividing your after-tax income into three broad categories:

- 50% for Needs: Covering essential expenses you cannot avoid.

- 30% for Wants: Allowing discretionary spending that enhances your lifestyle.

- 20% for Savings and Debt Repayment: Building financial security for the future.

This method resonates with many people because of its simplicity and flexibility. It provides a starting point for making sound financial decisions while still leaving room for enjoying life. Below, we delve into the details of this budgeting method and discuss how you can implement it successfully.

What is the 50/30/20 Budget Rule?

The 50/30/20 rule suggests that you allocate your net (after-tax) income into three primary buckets:

- Needs (50%): These are non-negotiable expenses—costs you must cover for survival and basic functioning. They include:

- Rent or mortgage payments

- Utilities (electricity, water, internet)

- Groceries and essential household supplies

- Transportation costs (car payments, fuel, public transit)

- Insurance premiums and minimum loan payments

- Wants (30%): This category covers all the non-essential expenses that improve your quality of life. They are discretionary and can include:

- Dining out and entertainment

- Subscriptions (streaming services, magazines)

- Travel and vacations

- Hobbies and leisure activities

- Savings and Debt Repayment (20%): This portion is dedicated to securing your financial future. It includes:

- Contributions to an emergency fund (ideally 3–6 months of living expenses)

- Retirement savings (401(k), IRA, etc.)

- Extra debt repayments (beyond the minimum required payments)

- Investments for long-term growth

This structure creates a balanced approach—ensuring you live comfortably in the present while also planning for the future.

Note: The percentages are guidelines. Depending on your personal situation, you might need to adjust them. For example, in high-cost-of-living areas, your “needs” might exceed 50%, requiring you to tighten spending on “wants” or find ways to boost income.

The Benefits of the 50/30/20 Rule

Simplicity and Ease of Use

One of the primary reasons why the 50/30/20 rule has gained popularity is its simplicity. Unlike complex spreadsheets with dozens of categories, this rule breaks down budgeting into three broad areas. This makes it easier to get started and stick to the plan, especially for individuals who are new to personal finance.

Encourages Financial Discipline

By setting clear limits on spending, the rule encourages discipline. You have to think critically about each purchase because you know that only a fixed portion of your income is available for discretionary spending. This mindset can help reduce impulse purchases and promote thoughtful spending.

Balances Enjoyment with Savings

Many budgeting methods force you to choose between living for today and saving for tomorrow. The 50/30/20 rule strikes a balance by allocating a significant portion of income to “wants” so you can enjoy life without neglecting savings. It helps foster a healthy relationship with money by acknowledging that while saving is crucial, it is also important to enjoy life’s pleasures responsibly.

Adaptability

No single budget fits everyone perfectly. The 50/30/20 rule is flexible enough to be adjusted based on individual needs. If you find that your essentials take up more than 50% of your income, you can tweak the percentages while still using the rule as a guiding framework.

Real-World Examples

Example 1: The Young Professional

Scenario:

Emma, a 28-year-old marketing professional, earns a net income of $4,000 per month. She lives in a mid-sized city where the cost of living is moderate.

Budget Breakdown:

- Needs (50%): $2,000

- Rent: $1,200

- Utilities: $150

- Groceries: $400

- Transportation: $250

- Insurance and Miscellaneous essentials: $0 (covered by employer benefits)

- Wants (30%): $1,200

- Dining out: $300

- Entertainment: $200

- Gym membership, subscriptions, hobbies: $300

- Travel savings, leisure activities: $400

- Savings and Debt Repayment (20%): $800

- Emergency fund: $300

- Retirement contributions: $300

- Extra debt repayment (student loan): $200

Emma uses budgeting apps to track her spending and finds that this structure keeps her finances balanced while still leaving room for social activities and future investments.

Example 2: The Family Budget

Scenario:

The Patel family has a combined net income of $6,000 per month. With two children and a mortgage, they have higher fixed expenses.

Budget Breakdown:

- Needs (50%): $3,000

- Mortgage: $2,000

- Utilities and Groceries: $600

- Transportation and Childcare: $400

- Wants (30%): $1,800

- Dining out and Entertainment: $700

- Family outings and vacations: $600

- Subscriptions and miscellaneous: $500

- Savings and Debt Repayment (20%): $1,200

- Emergency fund: $400

- Retirement and college savings: $500

- Debt repayments (credit cards): $300

By slightly adjusting discretionary spending and prioritizing saving for future educational costs, the Patels can maintain financial stability and prepare for long-term goals.

How to Implement the 50/30/20 Rule

Implementing the 50/30/20 rule involves a few strategic steps:

1. Calculate Your After-Tax Income

- Determine your net pay:

Use your pay stub to find your take-home pay (income after taxes, Social Security, and any other deductions). If you have additional deductions (such as retirement contributions automatically deducted), add those back in, as they will be allocated to the appropriate categories.

2. Track Your Expenses

- Record every expense for one month:

Use a budgeting app, spreadsheet, or even a simple notebook. Categorize each expenditure into “needs,” “wants,” or “savings/debt repayment.” - Review your bank and credit card statements:

This helps ensure you account for recurring payments and any forgotten expenses.

3. Create a Budget Allocation Table

A simple table can help you visualize your budget. Here is an example:

| Category | Percentage | Example Expenses | Monthly Amount (Based on $4,000) |

|---|---|---|---|

| Needs | 50% | Rent, utilities, groceries, transportation | $2,000 |

| Wants | 30% | Dining out, entertainment, subscriptions | $1,200 |

| Savings/Debt | 20% | Emergency fund, retirement, extra debt repayment | $800 |

Tip: Adjust the table values according to your own income and expense details.

4. Set Financial Goals

- Short-Term Goals:

These could be building an emergency fund, paying off credit card debt, or saving for a vacation. - Long-Term Goals:

Examples include retirement savings, buying a home, or funding your children’s education.

5. Automate Your Savings

- Set up automatic transfers:

Many banks allow you to schedule automatic transfers to your savings account. This “pay yourself first” strategy ensures that savings are prioritized over discretionary spending.

6. Regularly Review and Adjust Your Budget

- Monthly Check-ins:

Revisit your spending habits monthly. Life changes, and so should your budget. For instance, if your rent increases or you receive a bonus, adjust the percentages accordingly. - Use budgeting tools:

Apps like Mint, EveryDollar, or personal spreadsheets can help you monitor and adjust your expenses over time.

Actionable Financial Advice

Reduce Fixed Expenses

- Negotiate bills:

Call your service providers to see if you can secure lower rates on utilities or phone plans. - Downsize or refinance:

If housing costs are too high, consider refinancing your mortgage or moving to a more affordable area.

Control Discretionary Spending

- Prioritize what truly matters:

Differentiate between “wants” that genuinely add value to your life versus impulsive purchases. - Adopt a “cooling off” period:

Wait 24 hours before making non-essential purchases to reduce impulse spending.

Boost Your Savings

- Increase income streams:

Look for side gigs or freelance opportunities to supplement your income. - Invest early:

Even small amounts invested consistently can grow over time due to compound interest.

Educate Yourself

- Read reputable sources:

Stay informed by reading financial news, blogs from trusted experts, and resources like Investopedia and NerdWallet. - Consider professional advice:

If budgeting feels overwhelming, consider speaking to a certified financial planner who can tailor advice to your situation.

Limitations of the 50/30/20 Rule

While the 50/30/20 rule is an excellent starting point for many, it may not fit every situation perfectly.

High-Cost Living Areas

In cities where rent and other essential expenses consume more than 50% of your income, you might need to adjust the allocation. This could mean reducing the “wants” percentage or finding ways to lower your fixed costs.

Irregular Income

Freelancers or commission-based workers with irregular income may find it challenging to stick to fixed percentages every month. For such cases, it might be more useful to base your budget on an average monthly income over several months and adjust dynamically.

Personal Circumstances

Everyone’s financial goals and responsibilities differ. If you have significant debt or specific savings goals (like buying a home), you might choose to allocate more than 20% of your income toward savings and debt repayment. The 50/30/20 rule should be seen as a flexible framework rather than a rigid mandate.

Expert Insights on Budgeting

Financial experts widely endorse the 50/30/20 rule for its simplicity and balanced approach. For example:

- Harry Donoghue, a financial planner, calls it a “Goldilocks rule for budgeting” because it is neither too strict nor too lenient and works well as a foundational framework for managing your money.

- Rachel Cruze, a well-known personal finance expert, emphasizes that the key to success is not adhering rigidly to any one rule but using these percentages as a starting point that you can adjust as your financial situation evolves.

Experts agree that the real power of any budgeting system comes from consistency, regular review, and making adjustments that align with your evolving goals and lifestyle.

FAQs

How do I calculate my after-tax income?

Your after-tax income is the money you receive after deductions such as taxes, Social Security, and other withholdings. Check your pay stub to determine your net income. If your retirement contributions are deducted automatically, add them back in to allocate them properly according to your budget.

What if my essential expenses exceed 50% of my income?

In high-cost living areas, it is common for needs to take up more than 50% of your income. In such cases, consider reducing discretionary spending or finding ways to lower your fixed expenses. You can also adjust the percentages to suit your situation while still maintaining a focus on saving and responsible spending.

Can I modify the 50/30/20 rule to fit my personal goals?

Absolutely. The rule is a guideline, not a strict mandate. If you have heavy debt or aggressive savings goals, you might allocate more toward savings and debt repayment. The key is to use the rule as a starting point and tailor it to your unique financial needs.

What are some tools to help me stick to my budget?

Budgeting apps such as Mint, EveryDollar, and PocketGuard can automatically track and categorize your expenses. Many banks also offer budgeting tools integrated with your account. Regularly reviewing your budget using these tools can help you stay on track and make adjustments as needed.

How often should I review my budget?

It’s a good idea to review your budget at least once a month. However, if your income or expenses fluctuate frequently, you may want to check in more regularly—such as biweekly—to ensure you’re meeting your financial goals and adjust your allocations accordingly.

Conclusion

The 50/30/20 budgeting rule is a powerful yet simple framework that helps individuals balance essential living expenses, discretionary spending, and savings. Its simplicity, flexibility, and balanced approach make it an excellent starting point for anyone looking to gain control over their finances. By calculating your net income, tracking expenses, and regularly reviewing and adjusting your budget, you can build a solid financial foundation that allows you to meet your needs, enjoy your wants responsibly, and secure your future.

Remember, budgeting is not about restriction—it’s about empowering you to make informed financial decisions that align with your lifestyle and goals. Whether you’re a young professional, a family, or someone with irregular income, the 50/30/20 rule can serve as a stepping stone toward financial freedom. Start small, stay consistent, and adapt as needed. With discipline and regular review, you can make your money work for you and pave the way for a secure financial future.

By adopting a balanced approach and making slight adjustments based on your circumstances, you’ll find that managing your money becomes less of a chore and more of a path to financial empowerment. Happy budgeting!

Refrence: Using the 50-30-20 rule to power your household budget

[…] Financial experts regard the 50/30/20 rule as a balanced approach that provides a solid framework for managing finances. Read More. […]