Table of Contents

Introduction

Imagine losing the ability to work after an unexpected injury—or worse, leaving your loved ones with financial strain if a tragic accident occurs. Personal accident insurance offers a safety net, paying a lump sum or ongoing benefits when the unthinkable happens. In this guide, we’ll explore what personal accident insurance covers, how to choose the right policy, and why it’s increasingly essential in today’s risk-filled world.

What Is Personal Accident Insurance?

Personal accident insurance is a specialized policy that provides financial benefits if the policyholder suffers injury, disability, or death solely due to an accident. Unlike health insurance—which covers illness and general medical care—personal accident insurance focuses on accidents only, filling gaps such as loss of income or out-of-pocket costs not covered by health plans (Guardian Life).

Key features include:

- Lump-Sum or Periodic Payments: Depending on the policy, you may receive a one-time payout or regular benefit installments.

- Supplemental Coverage: Often paired with high-deductible health plans to cover copayments, ambulance fees, or rehabilitation costs (UnitedHealthOne).

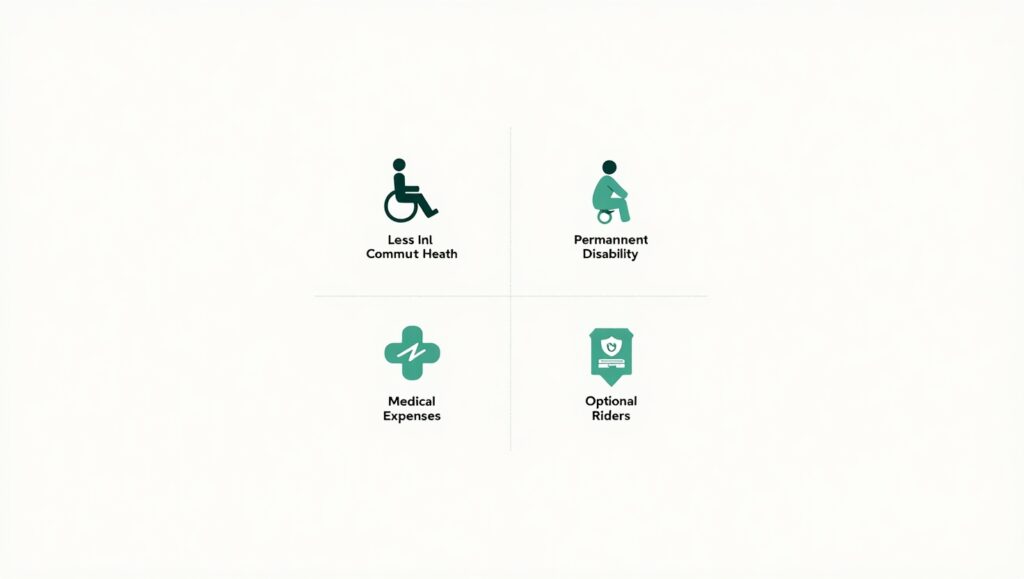

Key Coverage Components

Accidental Death Benefit

If an insured individual dies due to an accident, the policy pays a predetermined sum to the beneficiary. This benefit can range from a modest $25,000 plan to multi-hundred-thousand-dollar policies.

Permanent Total Disability Benefit

Covers permanent loss of bodily functions (e.g., loss of sight, hearing, or limb). Typical payouts match or exceed the death benefit, offering long-term financial support.

Medical Expense Reimbursement

Pays for accident-related medical expenses—such as hospital stays, X-rays, or physiotherapy—that may not be fully covered under your primary health plan (Guardian Life).

Additional Riders and Add-Ons

Policies may include optional riders for:

- Daily Hospital Cash: A fixed daily sum for each day hospitalized due to an accident.

- Child Education Benefit: Funds to cover a child’s education if a parent becomes disabled.

- Coma Benefit: Regular payments if the insured remains in a coma beyond a specified period.

Who Should Consider Personal Accident Insurance?

Individuals with High-Risk Occupations

Workers in construction, manufacturing, or transportation face elevated accident risk. A policy ensures they and their families are financially protected if a disabling incident occurs on the job.

Families and Dependents

Primary breadwinners may consider accident insurance to secure their family’s financial future against unforeseen accidents that compromise earning capacity.

Travelers and Adventure Enthusiasts

Frequent travelers or sports enthusiasts engaging in skiing, mountain biking, or other high-adrenaline activities benefit from coverage for emergencies abroad or during extreme sports.

How Premiums Are Calculated

Insurance providers assess several factors to determine your premium:

- Age and Health Status: Younger, healthier individuals typically pay lower rates.

- Occupation Risk Level: Jobs with higher accident incidence attract higher premiums.

- Coverage Amount: Larger benefit sums equal higher premiums.

- Add-On Riders: Additional benefits (e.g., hospital cash, education riders) increase cost.

- Geographic Location: Premiums vary by region, reflecting local healthcare costs and accident rates.

Market Trends and Data

The personal accident insurance sector is experiencing robust growth worldwide. Below is a comparison of global market size projections from reputable industry reports:

| Year | Market Size (USD Billion) | Source & Projection Period | CAGR (%) |

|---|---|---|---|

| 2023 | 158.7 | DataHorizzon Research; 2023–2033 | 5.7 (DataHorizzon Research) |

| 2024 | 152.0 | Dataintelo Report; 2024–2033 | 5.6 (Dataintelo) |

These figures highlight a strong upward trajectory, driven by increased consumer awareness and digital policy management innovations.

Case Study: Real-World Example

Scenario: A 35-year-old software engineer in New York purchases a $200,000 personal accident policy with riders for daily hospital cash ($100/day) and child education ($25,000).

- Accident: He sustains a severe leg fracture while mountain biking.

- Outcome:

- $200,000 lump sum for temporary total disability.

- $3,000 for a 30-day hospital stay.

- Funds cover physiotherapy, car modifications, and living expenses during recovery.

This case illustrates how layered benefits can mitigate both medical and lifestyle disruptions.

Expert Tips for Choosing a Policy

- Assess Your Risk Profile: Evaluate occupational hazards, hobbies, and family needs before selecting coverage amounts.

- Compare Multiple Insurers: Use comparison tools or consult an independent broker to find competitive premiums and policy features.

- Read the Fine Print: Note exclusions such as self-inflicted injuries, drug-related incidents, or high-risk sports without additional riders.

- Check Claim Settlement Ratios: A higher ratio indicates an insurer’s reliability in honoring claims.

- Opt for Cashless Facilities: If available, ensure the insurer has a network of hospitals for smoother cashless hospitalization.

How to File a Claim

- Immediate Notification: Inform the insurer within the stipulated period (usually 24–48 hours).

- Documentation: Submit the claim form, police or accident report, medical records, and proof of identity.

- Assessment: Insurance adjusters review the incident and may request additional evidence.

- Payout: Upon approval, benefits are disbursed as per policy terms—either as a lump sum or periodic payments.

Conclusion

Personal accident insurance is a crucial tool for safeguarding your financial well-being against unforeseen accidents. By understanding coverage components, premium determinants, and claim procedures, you can choose a policy that aligns with your risk profile and budget. Remember, the right accident insurance policy not only protects you but also provides peace of mind for you and your loved ones.

FAQs

What’s the difference between accidental death and permanent disability benefits?

- Accidental death benefit pays a lump sum if you die in an accident.

- Permanent total disability benefit pays if you survive but suffer a disability that prevents you from working.

Can I add riders to my personal accident policy?

Yes, most insurers offer riders such as daily hospital cash, child education benefits, and coma benefit for enhanced protection.

Does personal accident insurance cover illness-related hospitalization?

No, this insurance exclusively covers injuries from accidents. Illnesses are covered under health or critical illness insurance.

Are pre-existing conditions covered?

Generally, accidents affecting pre-existing injuries are excluded. Always review the policy’s exclusion section.

How much personal accident cover do I need?

Calculate based on your annual income (e.g., 5–10× your salary), outstanding debts, and family living expenses to ensure sufficient financial support.